WHAT IS A DEFERRED SALES TRUST?

A Deferred Sales Trust is a legal contract between an investor and a third-party trust in which the investor’s real property is sold to the trust in exchange for predetermined future payments, called installments, over an agreed upon period of time. Utilizing a Deferred Sales Trust, investors can defer capital gains taxes over time.

Deferred Sales Trusts provide an alternative to 1031 exchanges for deferring capital gains taxes on appreciated assets. Unlike exchange-based tax-deferment methods, Deferred Sales Trusts are an instance of a special kind of sale, called an “installment sale”, which can be used to defer capital gains taxes by breaking up payments on the sale over multiple installments. Unlike other installment sales, by using a third-party trust the Deferred Sales Trust arrangement can be used to reinvest your capital while indefinitely deferring your capital gains tax obligation.

Why You Should Defer Capital Gains Taxes

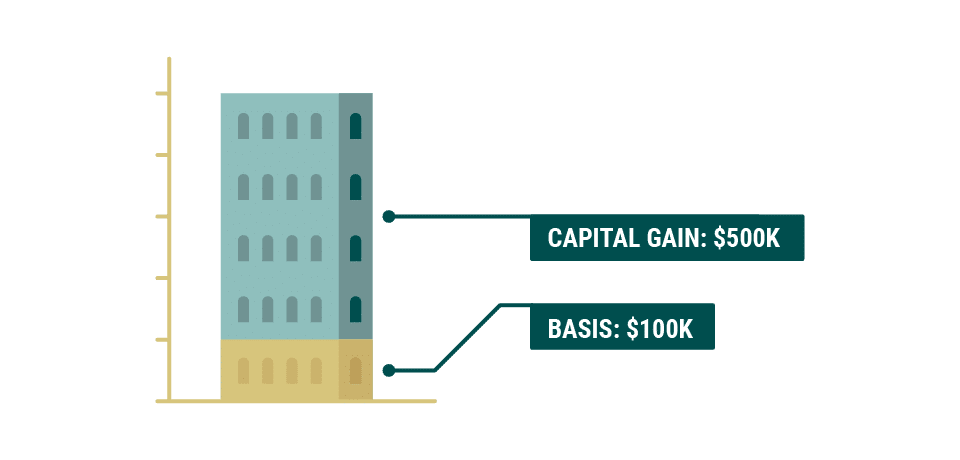

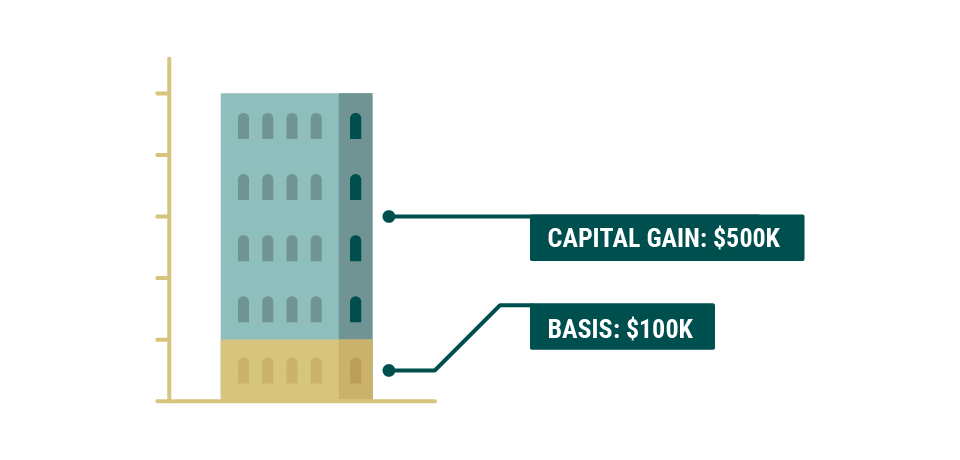

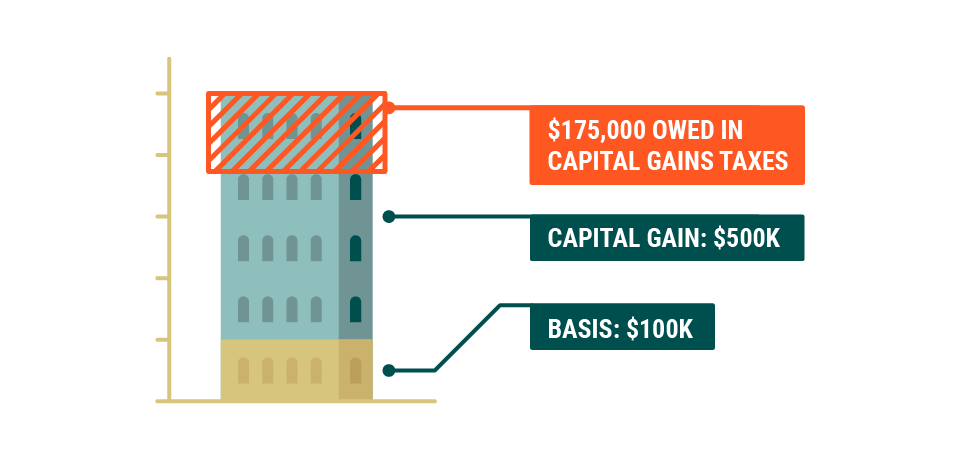

Your capital gain in any investment is the difference between the amount you sell it for and your “basis” in that investment. Typically, your basis in an investment is equal to its purchase price or fair market value at the time you acquired it.

Suppose you buy a property for $100,000, and then, many years later, you sell that property for $600,000. Since you’ve sold your property for more than you paid for it, you have made a capital gain. In this case, your basis is $100,000. Subtracting your basis from the property’s selling price, your capital gain therefore is $500,000 ($600,000 – $100,000 = $500,000).

Since you held onto this property for longer than a year, this capital gain counts as long-term capital gain. The federal tax rate on a long-term capital gain of $500,000 is 20%, or $100,000.1 After accounting for state and Medicare taxes, this rate can get up to 30-35% of your gain, or in this case, upwards of $175,000!

To avoid such a huge tax bill, you may be able to structure the sale or relinquishment of your investment property so that you defer having to pay capital gains taxes. A Deferred Sales Trust, or “installment sale” is such a tax-deferment tool for investors facing capital gains taxes.

What is a Deferred Sales Trust?

A Deferred Sales Trust is a legal method for deferring capital gains even though you sell your appreciated property instead of exchanging it.

In a 1031 exchange, 1033 exchange, or 721 exchange, you don’t actually sell your property. You swap it. Or, in the case of a 1033 exchange, you are compensated for the loss of your property to disasters like fire, earthquake, or Uncle Sam’s use of eminent domain.

Since in these cases you don’t sell something to buy something else, it makes sense for legal methods to be available for avoiding capital gains taxes. With the above processes, at no point do you really “gain”, so you shouldn’t have to be taxed on any gains.

But when you use a Deferred Sales Trust, or an “installment sale” (as provided for by section 453 of the U.S. Code) to defer capital gains taxes, you do indeed make a sale. The key difference between sales made as part of Deferred Sales Trust arrangements and ordinary sales concerns the method of payment.

With a Deferred Sales Trust, instead of the buyer paying you in one lump sum at the time of sale, the buyer instead agrees to pay you over multiple future installments. Depending on how these payments are organized, you can realize gain gradually over time or can even avoid realizing gain indefinitely.

The Deferred Sales Trust Process

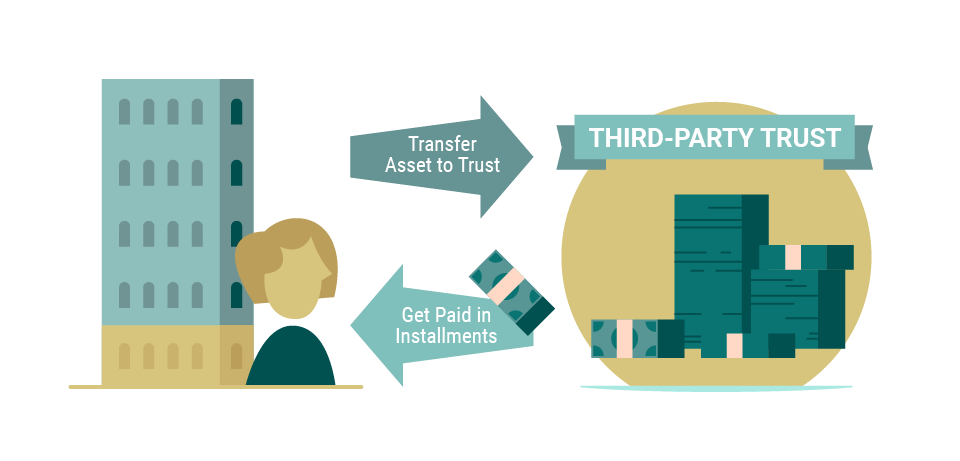

A Deferred Sales Trust arrangement is a specific version of an installment sale, as described in IRC 453. The process of using a Deferred Sales Trust begins with you, a property or business owner, transferring an asset to a trust that is managed by a third party on your behalf. The third party, acting as a trustee, sells your asset and agrees to pay you from the proceeds (or interest from the proceeds) over multiple future installments.

At first, since no payments are made in this transfer, you realize no capital gain, so owe nothing in capital gains taxes should the trustee sell the transferred asset. It is only as the trustee makes payments to you in installments that you may come to realize gain.

Section 453 of the Internal Revenue Code’ embodies the congressional recognition of one simple concept: taxpayers…should be permitted to return gain from the sale of property for deferred payment obligations as those obligations are satisfied rather than when the obligations are received.

John L. Ruppert2

So what happens when you start getting payments? How is this gradually realized gain calculated?

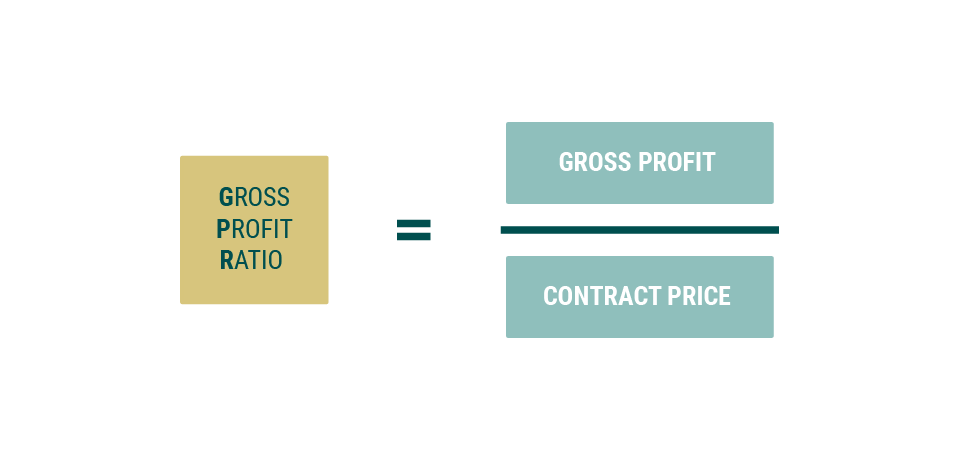

To figure out how much gain you realize once you begin to receive installments, first you calculate what the capital gains would have been were you to be paid in one lump sum at the time of sale. Using that calculation, you determine the “gross profit ratio”, which represents the proportion of your total sale which is gain.3 The amount of gain you realize with any payment is determined by the gross profit ratio.

Mathematically, the gross profit ratio is a fraction N such that multiplying N by the contract price (the total selling price minus any qualified indebtedness, including mortgage debt) equals the gain you would have realized were you to receive the full contract price at once at the time of sale.

Over time, you receive the installments at agreed-upon intervals. By multiplying each of these payments by the gross profit ratio, you get how much of that particular installment counts as gain, hence is subject to capital gains taxes.

Deferring Capital Gains Taxes with a Deferred Sales Trust

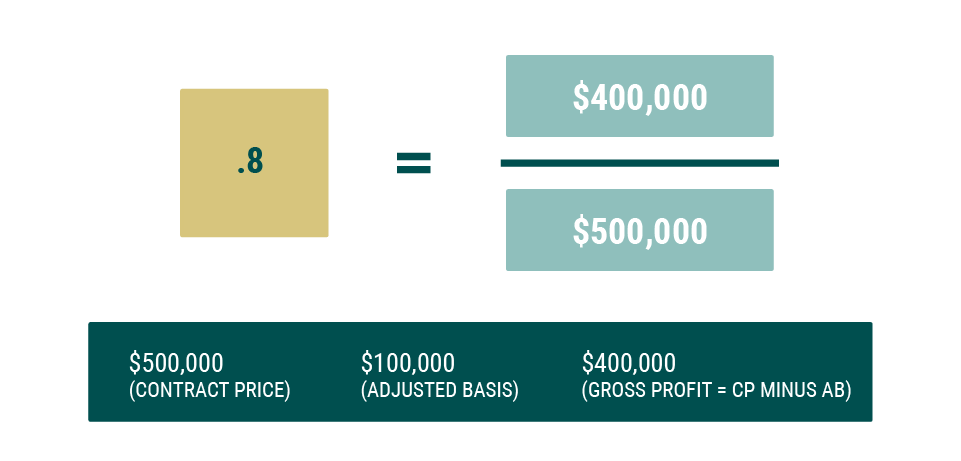

Suppose that you transfer an asset with a basis of $100,000 to a third-party trust and this asset is sold for $500,000 cash, to be held by the trust.

Now suppose the installment method of the contract says that you are to be paid $50,000 every six months. To calculate your gain every six months, you multiply your $50,000 payment by the gross profit ratio, which gives you $40,000. So on the total $100,000 you receive each year, you count as receiving $80,000 in gain, which is subject to capital gains taxes. Assuming a federal capital gains tax rate of 15% (since your gross profit equals $400,000), each year you will owe $12,000 in capital gains taxes. Things become slightly more complicated when one takes selling expenses and qualified indebtedness into account, but the calculation remains basically the same. Adding selling expenses makes the gross profit ratio smaller and adding qualified indebtedness makes the gross profit ratio larger.

So far we see that using a Deferred Sales Trust arrangement to defer capital gains can at least help you to break up the time frame in which you have to pay taxes on your capital gains, spreading your tax burden over several years rather than your having to pay it all in one lump sum.

Avoiding Capital Gains Taxes Indefinitely, Not Completely

Deferred Sales Trusts can be used not just to break up your capital gains tax bill, but also to defer capital gains taxes indefinitely.

Importantly, interest from an installment sale (that is, interest from investments made using the proceeds from the third party’s selling the transferred asset) does not count as any part of any payment of the agreed contract price.4 So, if your installments come just from interest on the sale, then in accepting that payment you still realize no gain whatsoever.

For example, suppose that you transfer your asset to the third party, which is then sold to acquire shares in an investment vehicle such as a REIT, which makes regular cash distributions. If the installment method is designed so that every six months you are to be paid from this cash flow and from nothing else, then for each taxable year you count as receiving no payments of the original contract price.

As long as none of the principal proceeds are returned to you as payment, then you have no payments made from the sale itself to multiply by the gross profit ratio, so you realize no gain. And so you owe no taxes on capital gains. In this way, you can use a Deferred Sales Trust to avoid realizing capital gains indefinitely.

You cannot, however, use a Deferred Sales Trust in accordance with section 453 to avoid paying capital gains altogether.

Once you receive a payment from the principal proceeds of your original sale, you will owe capital gains taxes on the proportion of that payment that counts as gain, given your gross profit ratio. The only way to avoid paying capital gains altogether would simply be to avoid receiving payments from the principal proceeds altogether.

If you ever want to receive any of the original profit from your sale, you will have to receive a corresponding portion of capital gain, at which point you incur a capital gains tax obligation.

Two Kinds of DSTs: Deferred Sales Trusts vs Delaware Statutory Trusts

What’s the difference between a Deferred Sales Trust and a Delaware Statutory Trust?

A Delaware Statutory Trust is a legal entity used to structure 1031-compatible real estate investment offerings. A Deferred Sales Trust is a legal arrangement between an investor and a third-party trust whereby one sells an appreciated asset while deferring one’s realization of capital gains.

Both kinds of “DSTs” can be used to defer capital gains taxes, but they do so in different ways.

Delaware Statutory Trusts can be used to help investors defer capital gains taxes as part of a 1031 exchange. Given their legal structure, shares in a Delaware Statutory Trust that holds real property can qualify as “like kind” to real estate held for investment. This is part of what enables one to use a 1031 exchange by acquiring qualifying shares in a Delaware Statutory Trust.

Deferred Sales Trusts, by contrast, provide an alternative to the 1031 exchange. Deferred Sales Trusts are simply another method for deferring capital gains taxes. So, they are not beholden to any of the timeline rules or property identification rules that constrain 1031 exchanges.

Does the IRS use the phrase ‘Deferred Sales Trust’?

The phrase “Deferred Sales Trust” actually is nowhere to be found in the Internal Revenue Code–the IRS itself does not use this lingo. Section 453 instead provides guidelines for deferring capital gains taxes using an “installment sale”. Robert Binkele trademarked the name “Deferred Sales Trust” to refer to one way of using a third-party trust as part of an installment sale. The practice of using third-party trusts in installment sales to defer capital gains taxes goes back several decades and extends beyond Binkele’s firm’s activity.

Pros and Cons of Deferred Sales Trusts

Let’s conclude by pointing out some of the pros and cons of Deferred Sales Trusts.

One potential positive feature of using an installment sale to defer your capital gains taxes rather than a 1031 exchange is that installment sales don’t come with the same strict guidelines that govern 1031 exchanges. In particular, in light of the Tax Cuts and Jobs Act of 2017, 1031 exchanges are restricted to real property, whereas Deferred Sales Trusts and other installment sale arrangements can be used to defer capital gains for any kind of asset.

Conversely, the IRS has provided little to no guidance on how to defer taxes using an installment sale.

The basic rationale behind why you don’t receive capital gain is that you are not profiting immediately from the sale made with a Deferred Sales Trust. Given this rationale, there are various constraints on how a Deferred Sales Trust must be organized so that no capital gains taxes are in fact realized.

- The third party to whom you transfer your asset generally cannot be a “related person” to you, such as a family member or a corporation in which you hold an interest.5,6 Except in special circumstances, if you attempt to set up a Deferred Sales Trust with a related person it will be viewed as a “sham trust” made just for the purposes of avoiding capital gains taxes, and will not be protected by the provisions in section 453.7

- As with the 1031 exchange, you, the seller, cannot at any point in the transfer of your asset be in constructive receipt of the proceeds from the third party’s sale of that asset. To successfully defer capital gains taxes, either the third party or the trust of which they are trustee must be the only party which receives cash in the sale of the transferred asset. This includes receipt of a bond which is payable on demand.8

This has been a general, informal introduction to Deferred Sales Trusts. As always, before attempting to carry out any important financial decision, investors should consult with a qualified tax or legal advisor regarding the specifics of their situation.

- https://www.irs.gov/taxtopics/tc409

- Ruppert, J. L. (1979). Section 453: Installment Sales Involving Related Parties or Trusts. DePaul L. Rev., 29,47

- 26 USC § 453(c)

- 26 USC § 453(l)(3)(b)(ii)

- 26 USC § 453(g)

- 26 USC § 453(h)(1)(C)

- See also: Ruppert, J. L. (1979). Section 453: Installment Sales Involving Related Parties or Trusts. DePaul L. Rev., 29, 47

- 26 USC § 453(f)(4)